AVANTAGES

Canadian Investment Review

CIIN

EVENTS

Webinars

AWARDS

Toggle navigation

Search

Newsletter

Magazine

My account

News

Benefits

Absence management

Communication

Disability management

Health benefits

Health/wellness

Legal issues

Other

Pensions

Capital accumulation plans

Governance/legislation

Retirement

Communication

Other

Investments

News

Partner Content

Expert Panel

DB

DC

Public Equities

Fixed income

Alternative investments

Investment Strategies

Research & Markets

Other

HR

Communication

Legal issues

Other

Expert Panel

Partner content

Partner Sites

Partner Series

Partner Education

Directories

Top stories in People Watch

Events

Webinars

Awards

Search>

News

Benefits

Absence management

Communication

Disability management

Health benefits

Health/wellness

Legal issues

Other

Pensions

Capital accumulation plans

Governance/legislation

Retirement

Communication

Other

Investments

News

Partner content

Expert Panel

DB

DC

Public Equities

Fixed income

Alternative investments

Investment Strategies

Research & Markets

Other

HR

Communication

Legal issues

Other

Expert Panel

Partner content

Sites

Series

Education

Roundtables

Directories

People Watch

Search>

Search

Top stories

Benefits Canada News

John Deere shareholders vote down anti-DEI resolution brought by conservative think tank

March 6, 2025

March 6, 2025

Retirement

National Institute on Ageing recognizing Bob Baldwin with lifetime achievement award

March 6, 2025

March 5, 2025

CIR News

BCI updates voting proxy guidelines, prioritizing ESG

March 6, 2025

March 5, 2025

Alternative investments

Caisse buys renewable energy operator, invests in $300M debt facility for internet company

By:

Staff

March 5, 2025

February 28, 2025

Benefits Canada Archive

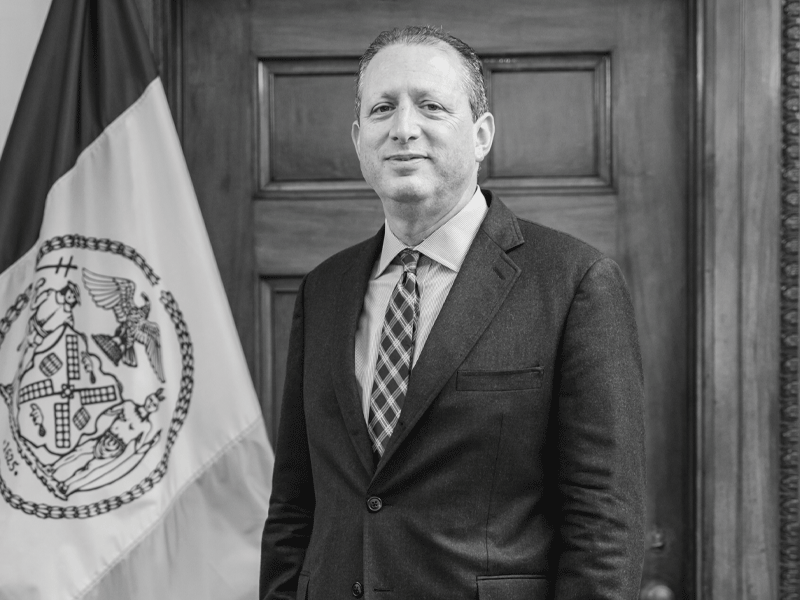

Making sustainable investments count at five New York City pension funds

By:

Bryan McGovern

December 13, 2024

December 12, 2024

Health/wellness

60% of Canadian employees want their employer to help with commuting costs: survey

By:

Staff

March 5, 2025

March 4, 2025

Defined benefit pensions

Estimated funded status of U.S. multi-employer DB plans rises to 97% in 2024: report

By:

Staff

February 28, 2025

February 24, 2025

CIR News

How are institutional investors reacting to tariff conflict between the U.S. and Canada?

By:

Bryan McGovern

March 4, 2025

March 6, 2025

Absence management

Nova Scotia expanding paid domestic violence leave to 5 days

By:

Staff

March 4, 2025

March 3, 2025

Benefits Canada News

Florida files suit against Target, claiming DEI initiatives ‘misled investors’

By:

Kate Payne, the Associated Press

February 28, 2025

February 27, 2025

Benefits Canada Archive

2024 CAP Suppliers Report: How can employers, pension industry support retirement needs of gig workers?

By:

Leah Golob

December 13, 2024

December 12, 2024

Retirement

36% of single Canadian employees believe they’ll never be able to retire: survey

By:

Staff

March 3, 2025

February 28, 2025

Health benefits

Manitoba becomes first province to join national pharmacare program with $219 million deal

By:

Sarah Ritchie, the Canadian Press

February 28, 2025

February 28, 2025

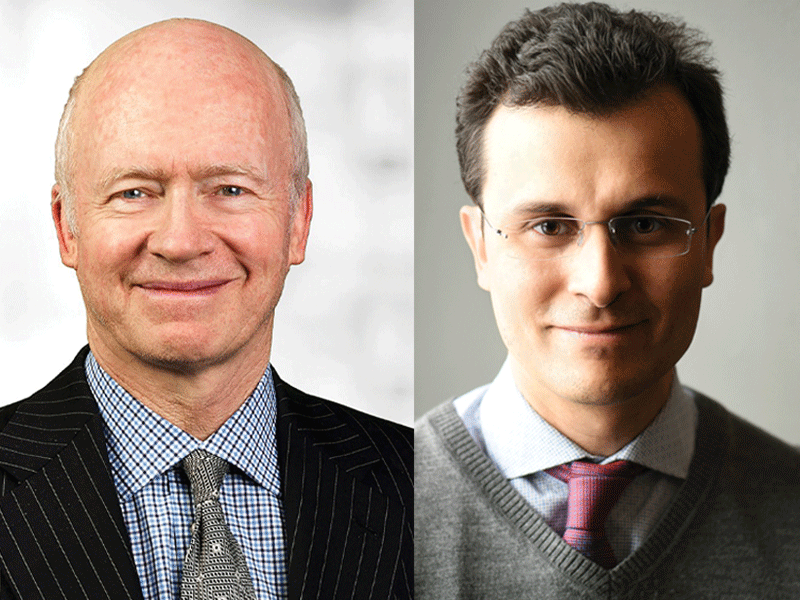

Kenneth MacDonald

Expert panel: How employers can prepare their benefits plans, support employees amid U.S. tariff threat

By:

Kenneth MacDonald

February 28, 2025

February 27, 2025

DC

DC investment options impacted by plan sponsor approach, external factors: report

By:

Staff

February 28, 2025

February 26, 2025

CIR News

Asset owners call on Canadian banks to stick with climate goals

By:

The Canadian Press

February 27, 2025

February 26, 2025

Benefits Canada News

Top 5 HR, benefits, pension and investment stories of the week

By:

Staff

February 28, 2025

February 27, 2025

Health/wellness

Telus Health building awareness of expression behind Black hair this Black History Month and beyond

By:

Lauren Bailey

February 27, 2025

February 26, 2025

CIR News

Caisse returns 9.4% in 2024, net assets grow to $473BN

By:

Staff

February 26, 2025

February 26, 2025

Benefits Canada News

Apple shareholders reject proposal to scrap company’s DEI programs

By:

Michael Liedtke, the Associated Press

February 26, 2025

February 26, 2025

Benefits Canada News

Caisse steering investments toward Quebec companies amid U.S. tariff threat

By:

Lauren Bailey

February 25, 2025

February 24, 2025

Benefits Canada Archive

Q&A with Marriott Hotels of Canada’s Candice Li

By:

Jennifer Paterson

December 13, 2024

December 12, 2024

CIR News

OMERS returns 8.3%, grows net assets to $138.2BN in 2024

By:

Staff

February 24, 2025

February 24, 2025

Benefits Canada Archive

Head to head: Should Canadian pension funds be incentivized to invest domestically?

By:

Benefits Canada

December 13, 2024

February 26, 2025

Retirement

Fewer millennials, gen Z employees on track to save for retirement: survey

By:

Staff

February 25, 2025

February 24, 2025

Alternative investments

Caisse selling 1.4% of common shares in Intact, IMCO writing down Northvolt investment: report

By:

Staff

February 21, 2025

February 19, 2025

Conference Coverage

2024 Defined Benefit Investment Forum: Canadian economy on high alert for impact of U.S. policy

By:

Bryan McGovern

January 30, 2025

January 28, 2025

Benefits Canada News

Spain government pushing through legislation for reduced workweek

By:

Staff

February 24, 2025

February 21, 2025

Health/wellness

Why standing all day at work can be hazardous to employee health

By:

Cathy Bussewitz, the Associated Press

February 21, 2025

February 21, 2025

Benefits Canada News

Employee belonging at core of DEI programs: expert

By:

Brooke Smith

February 21, 2025

February 27, 2025

DB

Ontario’s proposed long-term asset fund could introduce risks for both retail, institutional investors: PIAC

By:

Staff

February 20, 2025

February 19, 2025

Retirement

Survey finds 72% of U.K. employees in favour of responsibly invested pension plans

By:

Staff

February 20, 2025

February 21, 2025

Benefits Canada News

Top 5 HR, benefits, pension and investment stories of the week

By:

Staff

February 21, 2025

February 20, 2025

Retirement

FSRA’s third annual Pension Awareness Day promoting importance of retirement planning

By:

Bryan McGovern

February 20, 2025

February 19, 2025

Retirement

Canadians believe they’ll need $1.54 million to retire: survey

By:

Staff

February 20, 2025

February 20, 2025

CIR News

Institutional investors need to step up on climate as political momentum wavers: report

By:

Ian Bickis, the Canadian Press

February 19, 2025

February 19, 2025

Benefits Canada Archive

How Hydro Ottawa’s pre-retiree engagement strategy is supporting financial wellness, retirement readiness

By:

Blake Wolfe

December 13, 2024

December 12, 2024

Benefits Canada Experts

Kenneth MacDonald

Benefits Canada Experts

Expert panel: How employers can prepare their benefits plans, support employees amid U.S. tariff threat

Kim Siddall

Benefits Canada Experts

Expert panel: Chronic disease management, GLP-1s among 2025 health benefits trends

Gavin Benjamin

Benefits Canada Experts

Expert panel: Regulatory guidelines, geopolitical risk impacting pension plan sponsors in 2025

Katharine Coons

Benefits Canada Experts

Expert panel: Communication, technology shaping employers’ mental-health strategies in 2025

Canadian Investment Review Experts

Sebastien Betermier

Canadian Investment Review Experts

Expert panel: Building a more effective pension system for Canada’s private sector workers

George Athanassakos

Canadian Investment Review Experts

Expert panel: What are some CEO red flags for institutional investors to consider?

Les Marton

Canadian Investment Review Experts

Expert panel: Institutional investors should re-evaluate fees in ‘turbulent twenties’

Andrew Spence

Canadian Investment Review Experts

Expert panel: Cessation of real return bonds increases risk profile for Canadian pension fund model

From the current issue

Editorial: Challenges and opportunities amid an increasingly imbalanced generational divide

By:

Jennifer Paterson

How Hydro Ottawa’s pre-retiree engagement strategy is supporting financial wellness, retirement readiness

By:

Blake Wolfe

2024 CAP Suppliers Report: How can employers, pension industry support retirement needs of gig workers?

By:

Leah Golob

Making sustainable investments count at five New York City pension funds

By:

Bryan McGovern

More articles

Login Required