Canadian pension plans’ allocation to emerging market equities grew meaningfully in the five years between 2012 and 2016, according to the Canadian Institutional Investment Network; however, overall allocations remain small relative to other equity categories. That’s a missed opportunity, suggests Dáire Dunne, portfolio manager and director, multi-asset strategies, APAC, at Wellington Management. We asked him about investment opportunities in emerging market equities and why he thinks traditional benchmarks distract investors from many of the most interesting structural changes happening in markets today.

DÁIRE T. DUNNE, CFA

PORTFOLIO MANAGER AND DIRECTOR, MULTI-ASSET STRATEGIES, APAC, WELLINGTON MANAGEMENT

WHAT ARE THE PITFALLS OF TRACKING EMERGING MARKET INDICES RATHER THAN CONSTRUCTING AN ACTIVELY MANAGED EMERGING MARKET PORTFOLIO?

First, the benchmarks typically are very concentrated in particular areas. As an example, the two largest sectors in the MSCI Emerging Markets Index – technology and financials – currently contribute roughly 60% of the volatility. Second, currency contributes approximately 25% of that volatility. When you’re less anchored to the index, you can diversify some of that concentrated sector and currency exposure away.

In addition, indices tend to change really slowly over time and often reflect past winners, not future growth opportunities. We prefer to build a portfolio that seeks to look forward and get ahead of long-term structural changes.

WHY DO YOU BELIEVE ECONOMIC DEVELOPMENT IS STARTING TO SURPASS ECONOMIC GROWTH AS THE DOMINANT FORCE FOR STRUCTURAL CHANGE IN EMERGING MARKETS?

Policy dynamics are changing in emerging markets and this is creating new and different influences on financial markets. It’s not about maximizing output at all costs anymore. As people have become wealthier in emerging markets, they’re demanding better quality of life for themselves and for future generations. They’re demanding better education and better healthcare systems. We’re seeing a shift in emphasis from quantity of growth to quality of growth all around the emerging world. China is a wonderful example, with a raft of new policies geared towards improving the lives of people, improving the quality of the environment, and encouraging companies to make better long-term resource allocation decisions. There are big policy changes in India around affordable housing and infrastructure investment, and in Latin America, the Middle East and parts of Africa around the democratization of financial capital and education. These are fresh influences on financial markets. In the new policy world where development is the focus, it’s less about providing opportunities for deeply cyclical, growth-dominated sectors such as energy companies or banks, and more about providing tailwinds to companies that can encourage economic development over time, such as consumer services, automation, healthcare and infrastructure companies.

CAN YOU DESCRIBE SOME OF THE THEMES YOU’RE FOCUSING ON IN EMERGING MARKETS?

One is greater inclusiveness – improving the economic experience for as many people as possible. We’ve had a history in emerging markets of big disparities between the haves and have-nots, and a lot of policies today are about levelling that playing field. A deeply inclusive policy environment in healthcare in China and India, for example, is creating opportunities for hospitals, pharmaceutical companies, medical device companies and biotech companies. Sustainability is another area of focus for us. We’re interested in policy changes that will affect waste management, recycling, clean tech and alternative energy. Many of the world leaders in those areas are in emerging markets, and over half of clean tech spending globally happens in emerging markets. These opportunities are not widely understood or well represented in indices.

WHERE ARE YOU FINDING ATTRACTIVE OPPORTUNITIES RIGHT NOW?

To stay at the productivity frontier, emerging market countries are very enthusiastic about automation and robotics, and when we look across the globe, we’re seeing some of the greatest demand in this area coming out of emerging markets. China, Thailand, Indonesia and Mexico have all set very ambitious targets for robotic penetration within their manufacturing space. That’s one area.

Another is that, with a greater focus on the environmental cost of energy, policies are encouraging alternative energy sources and the more efficient use of energy. So we’re looking at opportunities related to renewables, recycling and energy efficiency under the umbrella of environmental consciousness.

Third, healthcare represents less than 3% of the MSCI Emerging Markets Index, and we think that is disproportionately low relative to the potential long-term opportunity. Our portfolio has an overweight exposure.

We’re also doing a lot of work on frontier markets because several countries in the Middle East, Asia and Africa are catching up fast to the traditional emerging market countries.

HOW DOES YOUR TOP-DOWN ANALYSIS WORK ALONGSIDE STOCK-LEVEL EXPERTISE TO BUILD MORE EFFECTIVE PORTFOLIOS?

We speak to governments, policymakers and academics as we travel around the emerging markets. Then we go hunting for themes related to the long-term structural changes we’ve identified. That’s when we speak with our investment colleagues internally who have deep specialization in particular sectors. At the moment, we have almost 60 career industry analysts spread all over the world looking at stocks, travelling to companies and conducting hundreds of meetings every year. It’s through external validation at the macro level with governments, policymakers and academics, and then through internal validation and travel to see companies, that we build our portfolio.

EMERGING MARKET EQUITIES ARE A GROWING BUT STILL VERY SMALL ALLOCATION WITHIN CANADIAN PENSION FUNDS – WHAT’S HOLDING PLAN SPONSORS BACK?

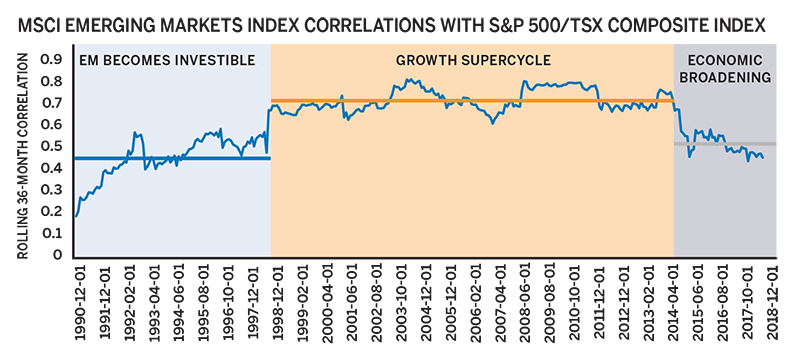

I don’t think there is a full appreciation for how emerging markets are evolving, becoming less commodity driven and more diversified from a portfolio perspective. The correlation between emerging market equities and Canadian equities, in Canadian dollar terms, has dropped from about 0.8 to about 0.5 (see chart). We think that offers a really interesting diversification opportunity. In addition, the transition away from some old economy sectors towards new economy sectors has changed the volatility profile of emerging markets. These sector compositional changes have impacted the volatility premium of emerging equities over developed market equities, pushing it to the lowest its been over the past 20 years. Lower volatility and lower correlations mean that emerging markets are contributing a much smaller level of risk at the overall portfolio level than many Canadian pension plans appreciate.

WHAT CAN CANADIAN PLAN SPONSORS GAIN FROM TAKING A FRESH, UNCONSTRAINED LOOK AT EMERGING MARKET EQUITIES?

If you’re unconstrained, you’re not restricted to the benchmark. You can widen the opportunity set. You can gain access to a richer set of potential alpha or stock-picking opportunities, and can get in front of some of these structural development trends. And you can allow for greater diversification within your overall plan. Ultimately, that should enable you to build more stable return streams over time. For more insights on emerging market investment-policy considerations specific to Canadian asset owners, visit us at www.wellington.com/Canada

Source: The data in this chart is from December 31, 1990 to April 30, 2018. Wellington Management calculated the rolling 36-month correlations based on return data from the S&P 500/TSX Composite Index and the MSCI Emerging Markets Index (CAD). PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS AND AN INVESTMENT CAN LOSE VALUE.

This material and/or its contents are current at the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the

express written consent of Wellington Management. This material is not intended to constitute investment advice or an offer to sell, or the solicitation of an offer to

purchase shares or other securities. Investors should always obtain and read an up-to-date investment services description or prospectus before deciding whether

to appoint an investment manager or to invest in a fund. Any views expressed herein are those of the author(s), are based on available information, and are subject

to change without notice. Individual portfolio management teams may hold different views and may make different investment decisions for different clients.

All investing involves risk. Principal risk considerations for investing in emerging markets equity include: currency risk, equity markets risk, foreign markets

risks, issuer-specific risk, liquidity risk, and smaller-capitalization stock risk.