How it works

One of the key benefits is how easy it is for plan members to understand, since the process is very straightforward:

Initial payment is calculated

Sun Life takes care of the math. Payments are based on (a) plan members’ total investment amount, (b) the number of years until selected maturity age, (c) a carefully estimated annual rate of return, (d) any annual regulatory minimums and maximums as applicable and (e) selected payment frequency.

Payments are refreshed each year

At the start of each year payments are refreshed based on plan members’ remaining account balance and taking into account actual investment performance, withdrawals and deposits made the previous year.

Regular income until chosen maturity age

Everything is automated for the plan member, and they don’t need to make any adjustments - unless they want to.

The underlying investment is designed for retirement

The underlying investment in Sun Life MyRetirement income is specifically designed for individuals in retirement. The asset allocation and underlying assets strike the right balance between:

- generating an adequate level of return to make the money last to the age of maturity (and help maintain standard of living) and

- minimizing the investment risk to minimize fluctuation in payments.

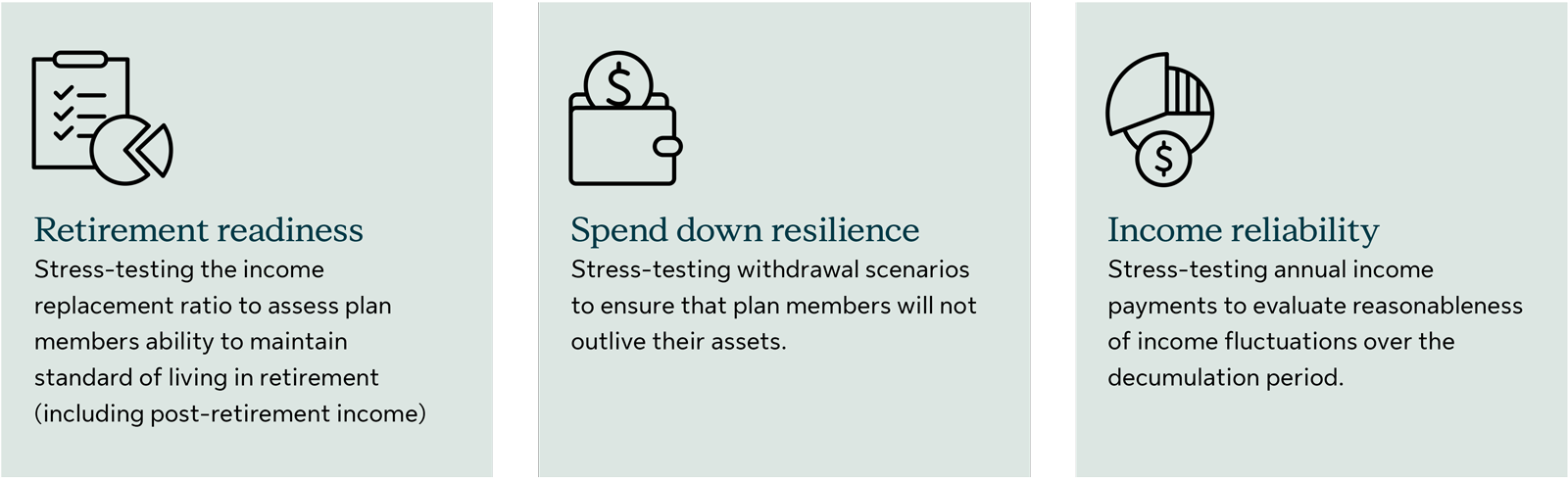

It has been stress-tested in several ways to ensure it will deliver the best possible retirement incomes:

We know that more than 50% of plan members are concerned about the impact inflation will have on their retirement savings3. The fund has a strategic weight of 41.5% in various kinds of equity (including liquid and direct alternatives), providing a potential hedge against inflation, and 58.5% in fixed income, including specialty asset classes such as private fixed income and commercial mortgages.

The underlying investment has a number of additional advantages:

Managed by experts

Portfolio managers specialize in multi-asset solutions and complex asset allocation

Broader diversification

Diversified by style, region and asset class, including a combination of active & passive. Access to specialty asset classes that every day investors cannot get (such as direct real estate, infrastructure and liquid alternatives)

Multi-manager

Not just one manager… the team chooses the manager they believe is best in each asset class

Adapts to short-term conditions

Tactical overlay allows portfolio managers to shift allocations, capitalizing on short term market opportunities

Continual enhancements

The team looks for ways to enhance the portfolio by reevaluating the asset mix, underlying asset classes and investment managers

Sponsored by: